Journal of Shanghai University >

Shadow banking business, corporate governance and analysts' earnings forecasts

Received date: 2020-11-12

Online published: 2021-10-22

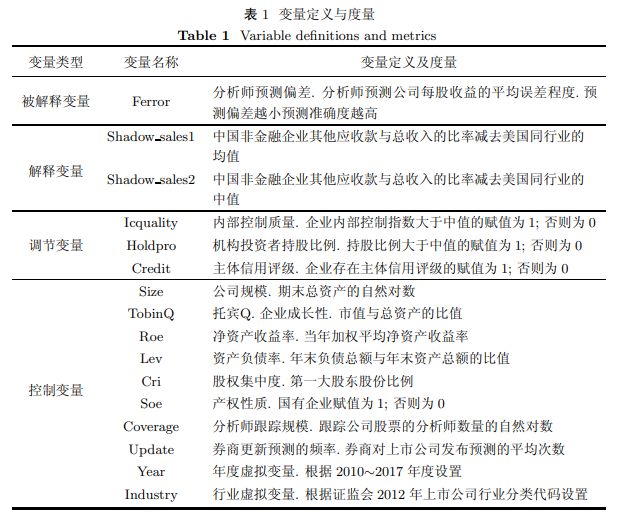

Shadow banking activities have received extensive attention from academia and supervisory bodies. To study this issue, this paper used data samples on China's listed non-financial enterprises from 2010 to 2017, obtained from the Standard & Poor's Compustat Global database, to examine the relationship between the shadow banking business of non-financial enterprises and the accuracy of analysts' predictions. This study found that the greater the participation of non-financial enterprises in shadow banking, the higher the error rate of analysts' predictions—that is, the lower their prediction accuracy. Further analysis showed that the above relationship was more significant in enterprises whose internal control quality, shareholding ratio of institutional investors, and credit ratings were low; moreover, it was observed that the shadow banking business of non-financial enterprises can increase the accrued earnings management of the enterprises and reduce the quality of information disclosure. The results remained robust after the measures of explanatory variables and explained variables were replaced. This study not only contributes to the literature on the economic consequences of the shadow banking business of non-financial enterprises and the accuracy of analysts' predictions, but also offers important guidance to analysts on being alert to the risks of shadow banking and market regulation.

Endian YAN , Sijia GAO . Shadow banking business, corporate governance and analysts' earnings forecasts[J]. Journal of Shanghai University, 2021 , 27(5) : 972 -982 . DOI: 10.12066/j.issn.1007-2861.2306

| [1] | Han X, Tian G N, Li J J. Shadow banking business and financial structure of non-financing enterprises—empirical evidence from Chinese listed companies[J]. Studies of International Finance, 2017(10): 44-54. |

| [2] | Lu S R, Guo X N, You Y X. Shadow banking, misallocation of credit resources and China's economic fluctuations[J]. Studies of International Finance, 2019(4): 66-76. |

| [3] | Wang Y Q, Liu Z H, Li C, et al. Non-financial firms as banks: identifying shadow banking activities in China[J]. Management World, 2015(12): 24-40. |

| [4] | Yan E D, Sun A Q, Chu Y Q, et al. Shadow banking, auditor choice and auditing characteristics: evidence from China[J]. Nankai Business Review, 2018(5): 117-127; 138. |

| [5] | Li J J, Han X. Non-financial enterprises' shadow banking business and operating risk[J]. Economic Research Journal, 2019, 54(8): 21-35. |

| [6] | Qiu X, Zhou Q L. Shadow banking and monetary policy transmission[J]. Economic Research Journal, 2014, 49(5): 91-105. |

| [7] | Gao B, Chen X D, Li C. Banking property rights heterogeneity, shadow banking and the effectiveness of monetary policy[J]. Economic Research Journal, 2020, 55(4): 53-69. |

| [8] | Gennaioli N, Shleifer A, Vishny R. Neglected risks, financial innovation and financial fragility[J]. Journal of Financial Economics, 2012, 104(3): 452-468. |

| [9] | Lang M H, Lins K V, Miller D P. ADRs, analysts and accuracy: does cross listing in the United States improve a firm's information environment and increase market value?[J]. Journal of Accounting Research, 2003, 41(2): 317-345. |

| [10] | Wang P N, Luo H. Deregulation on short selling constraint and analysts’ forecast behavior: evidence from quasi natural experiment of China[J]. Journal of Financial Research, 2017(11): 191-206. |

| [11] | Brown L D, Richardson G D, Schwager S C. An informational interpretation of financial analyst superiority in forecasting earnings[J]. Journal of Accounting Research, 1987, 25(1): 49-67. |

| [12] | Wang Y T, Wang Y C. Does earnings preannouncement information impose effects on the forecast behavior of financial analysts?[J]. Journal of Financial Research, 2012(6): 193-206. |

| [13] | Huang J, Huang C, Wei H Q, et al. Does short selling improve analysts' earnings forecast quality: evidence from China's securities margin trading[J]. Nankai Business Review, 2018, 21(2): 135-148. |

| [14] | Li Y Q, Yao Y. R & D narrative disclosure: is talk more really useless?—textual analysis based on analysts' forecast[J]. Accounting Research, 2020(2): 26-42. |

| [15] | He X Q, Yin C P. Does strategic deviance influence analysts' earnings forecasts: an empirical study based on Chinese security markets[J]. Nankai Business Review, 2018, 21(2): 149-159. |

| [16] | Tan S T, Gan S L, Kan S. Does media coverage decrease the analysts' forecast error?[J]. Journal of Financial Research, 2015(5): 192-206. |

| [17] | Kumar A. Self-selection and the forecasting abilities of female equity analysts[J]. Journal of Accounting Research, 2010, 48(2): 393-435. |

| [18] | Bradley D, Gokkaya S, Liu X. Before an analyst becomes an analyst: does industry experience matter?[J]. The Journal of Finance, 2017, 72(2): 751-792. |

| [19] | Clement M B. Analyst forecast accuracy: Do ability, resources, and portfolio complexity matter?[J]. Journal of Accounting and Economics, 1999, 27(3): 285-303. |

| [20] | Yin Z H, Li Y, Jiang X Y. Female analysts' coverage and stock return synchronicity[J]. Journal of Financial Research, 2015(11): 175-189. |

| [21] | Xie G H, Hao Y, Li S L. Industry concentration, analysts' industry expertise and forecast accuracy[J]. Foreign Economics & Management, 2019, 41(2): 125-138. |

| [22] | Zhou G L, Meng Q X, Wu K W, et al. The information effect of securities analysts' hometown network capital[J]. Journal of Finance and Economics, 2020, 46(5): 111-124. |

| [23] | Barron O E, Byard D, Yu Y. Earnings announcement disclosures and changes in analysts' information[J]. Contemporary Accounting Research, 2016, 34(1): 343-373. |

| [24] | Dong W, Chen J, Chen H W. Does internal control quality affect analysts' behavior?: evidence from China[J]. Journal of Financial Research, 2017(12): 191-206. |

| [25] | Ashbaugh-Skaife H, Collins D W, Kinney W R, et al. The effect of SOX internal control deficiencies and their remediation on accrual quality[J]. The Accounting Review, 2008, 83(1): 217-250. |

| [26] | Feng M, Li C, McVay S. Internal control and management guidance[J]. Journal of Accounting and Economics, 2009, 48(2/3): 190-209. |

| [27] | Tan J S, Lin Y C. The governance role of institutional investors in information disclosure: evidence from institutional investors' corporate visits[J]. Nankai Business Review, 2016, 19(5): 115-126; 138. |

| [28] | Liu Q Q, Chen S S. Cast sheep's eyes: managements' guidance and analysts' earnings forecast errors[J]. Nankai Business Review, 2019, 22(5): 207-224. |

| [29] | Gallemore J, Gipper B, Maydew E. Banks as tax planning intermediaries[J]. Journal of Accounting Research, 2019, 57(1): 169-209. |

| [30] | Lin W F, Zhao Z K, Liu Y F, et al. Can rating information of bond market improve stock market information quality?—evidence from analysts' forecasts[J]. Journal of Financial Research, 2020(4): 166-185. |

| [31] | Francis J R, Neuman S S, Newton N J. Does tax planning affect analysts' forecast accuracy?[J]. Contemporary Accounting Research, 2019, 36(4): 1-32. |

| [32] | Yan E D, Xie J J. Supply chain relationship, information superiority and shadow banking—empirical evidence based on listed non-financial companies[J]. Management Review, 2021, 33(1): 291-300; 329. |

/

| 〈 |

|

〉 |