收稿日期: 2020-11-12

网络出版日期: 2021-10-22

基金资助

国家自然科学基金资助项目(71632006);教育部人文社会科学研究项目(20YJC790159)

Shadow banking business, corporate governance and analysts' earnings forecasts

Received date: 2020-11-12

Online published: 2021-10-22

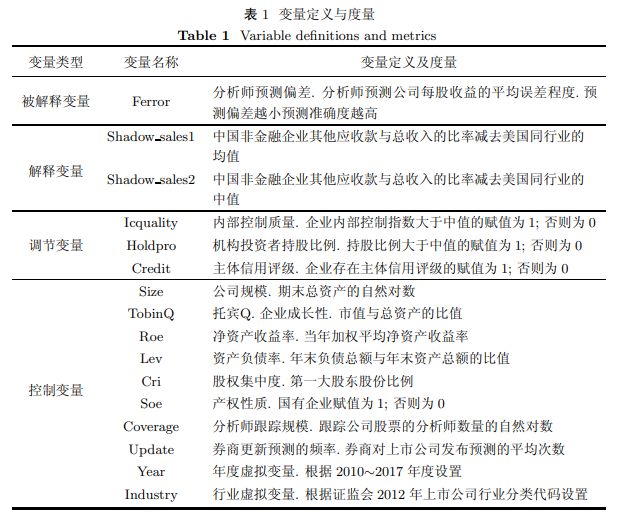

影子银行业务受到学术界和监管部门的广泛关注. 利用标准普尔的 Compustat Global 企业数据库提供的 2010~2017 年我国上市非金融企业样本, 从非金融企业的影子银行业务与分析师预测准确度的关系进行研究. 结果发现, 非金融企业的影子银行业务量越大, 分析师预测偏差越大, 即预测准确度越低. 进一步分析后发现, 上述关系在内部控制质量低、机构持股比例低和信用等级低的企业更显著, 并且非金融企业的影子银行业务会增加企业的应计盈余管理, 降低信息披露质量. 最后, 替换了解释变量和被解释变量, 并考察了内生性问题, 结果依然稳健. 因此, 该研究不仅丰富了非金融企业参与影子银行业务的经济后果和分析师预测准确度方面的相关文献, 还对分析师警惕影子银行业务的风险和市场监管具有重要指导意义.

颜恩点, 高思佳 . 影子银行业务、公司治理与分析师盈余预测[J]. 上海大学学报(自然科学版), 2021 , 27(5) : 972 -982 . DOI: 10.12066/j.issn.1007-2861.2306

Shadow banking activities have received extensive attention from academia and supervisory bodies. To study this issue, this paper used data samples on China's listed non-financial enterprises from 2010 to 2017, obtained from the Standard & Poor's Compustat Global database, to examine the relationship between the shadow banking business of non-financial enterprises and the accuracy of analysts' predictions. This study found that the greater the participation of non-financial enterprises in shadow banking, the higher the error rate of analysts' predictions—that is, the lower their prediction accuracy. Further analysis showed that the above relationship was more significant in enterprises whose internal control quality, shareholding ratio of institutional investors, and credit ratings were low; moreover, it was observed that the shadow banking business of non-financial enterprises can increase the accrued earnings management of the enterprises and reduce the quality of information disclosure. The results remained robust after the measures of explanatory variables and explained variables were replaced. This study not only contributes to the literature on the economic consequences of the shadow banking business of non-financial enterprises and the accuracy of analysts' predictions, but also offers important guidance to analysts on being alert to the risks of shadow banking and market regulation.

| [1] | Han X, Tian G N, Li J J. Shadow banking business and financial structure of non-financing enterprises—empirical evidence from Chinese listed companies[J]. Studies of International Finance, 2017(10): 44-54. |

| [2] | Lu S R, Guo X N, You Y X. Shadow banking, misallocation of credit resources and China's economic fluctuations[J]. Studies of International Finance, 2019(4): 66-76. |

| [3] | Wang Y Q, Liu Z H, Li C, et al. Non-financial firms as banks: identifying shadow banking activities in China[J]. Management World, 2015(12): 24-40. |

| [4] | Yan E D, Sun A Q, Chu Y Q, et al. Shadow banking, auditor choice and auditing characteristics: evidence from China[J]. Nankai Business Review, 2018(5): 117-127; 138. |

| [5] | Li J J, Han X. Non-financial enterprises' shadow banking business and operating risk[J]. Economic Research Journal, 2019, 54(8): 21-35. |

| [6] | Qiu X, Zhou Q L. Shadow banking and monetary policy transmission[J]. Economic Research Journal, 2014, 49(5): 91-105. |

| [7] | Gao B, Chen X D, Li C. Banking property rights heterogeneity, shadow banking and the effectiveness of monetary policy[J]. Economic Research Journal, 2020, 55(4): 53-69. |

| [8] | Gennaioli N, Shleifer A, Vishny R. Neglected risks, financial innovation and financial fragility[J]. Journal of Financial Economics, 2012, 104(3): 452-468. |

| [9] | Lang M H, Lins K V, Miller D P. ADRs, analysts and accuracy: does cross listing in the United States improve a firm's information environment and increase market value?[J]. Journal of Accounting Research, 2003, 41(2): 317-345. |

| [10] | Wang P N, Luo H. Deregulation on short selling constraint and analysts’ forecast behavior: evidence from quasi natural experiment of China[J]. Journal of Financial Research, 2017(11): 191-206. |

| [11] | Brown L D, Richardson G D, Schwager S C. An informational interpretation of financial analyst superiority in forecasting earnings[J]. Journal of Accounting Research, 1987, 25(1): 49-67. |

| [12] | Wang Y T, Wang Y C. Does earnings preannouncement information impose effects on the forecast behavior of financial analysts?[J]. Journal of Financial Research, 2012(6): 193-206. |

| [13] | Huang J, Huang C, Wei H Q, et al. Does short selling improve analysts' earnings forecast quality: evidence from China's securities margin trading[J]. Nankai Business Review, 2018, 21(2): 135-148. |

| [14] | Li Y Q, Yao Y. R & D narrative disclosure: is talk more really useless?—textual analysis based on analysts' forecast[J]. Accounting Research, 2020(2): 26-42. |

| [15] | He X Q, Yin C P. Does strategic deviance influence analysts' earnings forecasts: an empirical study based on Chinese security markets[J]. Nankai Business Review, 2018, 21(2): 149-159. |

| [16] | Tan S T, Gan S L, Kan S. Does media coverage decrease the analysts' forecast error?[J]. Journal of Financial Research, 2015(5): 192-206. |

| [17] | Kumar A. Self-selection and the forecasting abilities of female equity analysts[J]. Journal of Accounting Research, 2010, 48(2): 393-435. |

| [18] | Bradley D, Gokkaya S, Liu X. Before an analyst becomes an analyst: does industry experience matter?[J]. The Journal of Finance, 2017, 72(2): 751-792. |

| [19] | Clement M B. Analyst forecast accuracy: Do ability, resources, and portfolio complexity matter?[J]. Journal of Accounting and Economics, 1999, 27(3): 285-303. |

| [20] | Yin Z H, Li Y, Jiang X Y. Female analysts' coverage and stock return synchronicity[J]. Journal of Financial Research, 2015(11): 175-189. |

| [21] | Xie G H, Hao Y, Li S L. Industry concentration, analysts' industry expertise and forecast accuracy[J]. Foreign Economics & Management, 2019, 41(2): 125-138. |

| [22] | Zhou G L, Meng Q X, Wu K W, et al. The information effect of securities analysts' hometown network capital[J]. Journal of Finance and Economics, 2020, 46(5): 111-124. |

| [23] | Barron O E, Byard D, Yu Y. Earnings announcement disclosures and changes in analysts' information[J]. Contemporary Accounting Research, 2016, 34(1): 343-373. |

| [24] | Dong W, Chen J, Chen H W. Does internal control quality affect analysts' behavior?: evidence from China[J]. Journal of Financial Research, 2017(12): 191-206. |

| [25] | Ashbaugh-Skaife H, Collins D W, Kinney W R, et al. The effect of SOX internal control deficiencies and their remediation on accrual quality[J]. The Accounting Review, 2008, 83(1): 217-250. |

| [26] | Feng M, Li C, McVay S. Internal control and management guidance[J]. Journal of Accounting and Economics, 2009, 48(2/3): 190-209. |

| [27] | Tan J S, Lin Y C. The governance role of institutional investors in information disclosure: evidence from institutional investors' corporate visits[J]. Nankai Business Review, 2016, 19(5): 115-126; 138. |

| [28] | Liu Q Q, Chen S S. Cast sheep's eyes: managements' guidance and analysts' earnings forecast errors[J]. Nankai Business Review, 2019, 22(5): 207-224. |

| [29] | Gallemore J, Gipper B, Maydew E. Banks as tax planning intermediaries[J]. Journal of Accounting Research, 2019, 57(1): 169-209. |

| [30] | Lin W F, Zhao Z K, Liu Y F, et al. Can rating information of bond market improve stock market information quality?—evidence from analysts' forecasts[J]. Journal of Financial Research, 2020(4): 166-185. |

| [31] | Francis J R, Neuman S S, Newton N J. Does tax planning affect analysts' forecast accuracy?[J]. Contemporary Accounting Research, 2019, 36(4): 1-32. |

| [32] | Yan E D, Xie J J. Supply chain relationship, information superiority and shadow banking—empirical evidence based on listed non-financial companies[J]. Management Review, 2021, 33(1): 291-300; 329. |

/

| 〈 |

|

〉 |